Türkiye’s financial sector needs to prepare for intensifying climate-related risks

Türkiye’s geographic location, population density and distribution, and socioeconomic factors make it highly vulnerable to the impacts of climate change and other environmental and natural hazards, as detailed in the World Bank’s Türkiye Country Climate and Development Report (CCDR). Concerns are also rising about climate change exacerbating water stress and food security issues. Regional ‘green’ initiatives, such as the European Union’s Green Deal, are increasing the pressure to act fast to get to a net zero future. However, the transition to decarbonization also comes with risks as changes in policy need to be absorbed and carefully managed.

What does this mean for Türkiye’s financial sector and especially its banks, considering they are the largest part of the domestic financial system? Generally speaking, climate physical and transition risks have the potential to undermine the profitability and solvency of financial institutions if they increase non-performing loans (NPLs) in affected regions and economic sectors. Regulators and financial institutions need to explore these implications and take action to shore up the banking sector’s resilience.

Implications of intensifying physical risks for Turkish banks

Türkiye is one of the most vulnerable countries to climate change within the OECD. In 2021 alone, the country experienced 107 floods, 66 forest fires, 16 snowstorms and 39 landslides, according to the Disaster and Emergency Management Authority (AFAD) of Türkiye. Meanwhile, the annual probability of flash floods, droughts, extreme heat events, and wildfires is projected to increase with growing climate change.

Such events can impact the economy and banking sector through multiple channels. For example, heat stress is projected to reduce labor productivity, while drought can impact the output of the agricultural sector, as well as other water users, including those in urban areas. Such risks are compounded by other shocks, such as earthquakes, pandemics, and spikes in international food prices.

Turkish banks are exposed to significant physical risks given their geographically concentrated loan portfolios. For example, about 42% of all bank loans are concentrated in Istanbul, Tekirdag, and Kocaeli, which are at high risk of drought and earthquake. Tourism sector loans are mostly concentrated in Antalya and Muğla, which were hit by the massive forest fires in 2021. Analysis from the Van earthquake in 2011 shows that natural disasters can have substantial impacts on NPLs.

Transition risks could be significant

Exposure to transition-related risks can be estimated through banks’ lending to high carbon-emitting sectors. The top five carbon-emitting sectors—energy, manufacturing, transport, wholesale trade, and agriculture—have about a 49% share of total bank credit in Türkiye. The energy and agriculture sectors show relatively high ratios of NPLs. At the same time, manufacturing, wholesale trade, and transportation constitute about 49% of GDP and are significant export revenue generators for Türkiye. The high carbon intensity of those sectors exposes them and the institutions that finance them to transition risk. For instance, the EU’s Carbon Border Adjustment Mechanism (CBAM), which is expected to become effective from October this year, would impose higher tariffs for selected imported products based on their carbon footprint, rendering Turkish export goods potentially less competitive. As the EU is Türkiye’s most important trading partner, with a 41% share in Türkiye’s exports, the Türkiye CCDR analysis shows strong reductions in exports in selected sectors, depending on the design of CBAM, with an indirect price impact across sectors.

Role of regulators and supervisors

Banks (and other financial institutions) need to be able to assess, manage, and mitigate the risks arising from climate and environmental issues.

For that to be possible, Turkish regulators and supervisors need to continue building internal capacity to integrate climate risk throughout the supervisory framework, as emphasized in an earlier World Bank report, Unlocking Green Finance in Turkey. The Banking Regulation and Supervision Agency’s (BRSA) strategic plan is encouraging, but more needs to be done.

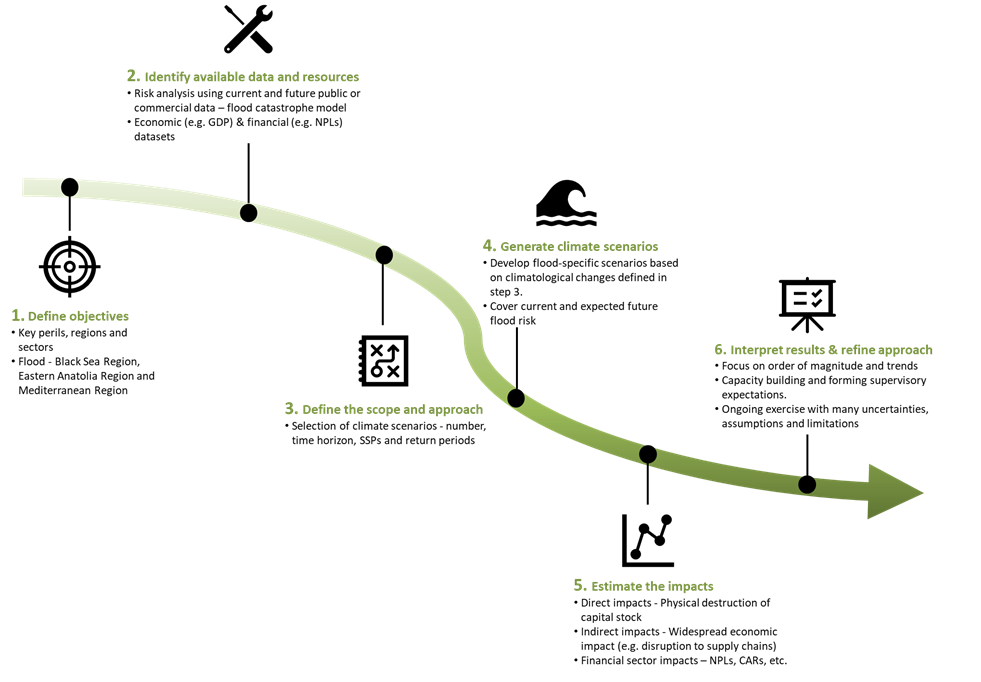

Key steps to be taken include using event- or scenario-based climate stress tests to assess risks. Given Türkiye’s large exposure to physical and transition risk, both dimensions are of relevance for the financial sector. Stress-testing exercises usually include a macroeconomic or microeconomic approach, as conducted by the World Bank in Colombia and jointly with the International Monetary Fund in the Philippines and Mexico. Accounting for the international finance and trade dimension is especially relevant, given Türkiye’s close ties to the EU. The chart below illustrates the key steps for a physical climate financial risk assessment, using the example of flood risks.

Key steps for a climate-financial risk assessment for the example of flood risk. Source: Authors.

Key steps for a climate-financial risk assessment for the example of flood risk. Source: Authors.

Insights from the risk assessments could then guide the establishment of guidelines on integrating climate risk in risk management, governance, data and disclosure practices, and supervisory scoring models and approaches, and the assessment of how to embed climate risk in existing regulations. Such guidance will support a portfolio shift away from climate risky assets towards green and resilient investments, therewith stimulating change in the real economy. The World Bank stands ready to support BRSA and other financial sector regulators in those efforts.

This blog was originally published on World Bank Blogs - Link here