Enhanced financial services for improved climate resilience: Some insights from the economic theory

The global protection gap related to climate shocks and disasters keeps growing. According to the insurance industry, this protection gap worldwide is estimated at 67 percent in 2023: this means that only 33 percent of the direct economic costs of natural hazards, estimated at USD357 billion in 2023, were insured. This protection gap is even wider in emerging markets and developing economies, where it can exceed 90 percent. Climate shocks and extreme weather events not only reduce the welfare of vulnerable households, but such disasters are also threatening to push more than 130 million people into extreme poverty by 2030.

Improving access to financial services for resilience has become a policy question among development partners and developing countries. For example, insurance can help vulnerable households protect their livelihood and assets against disasters and climate shocks. One prominent public intervention has been the provision of insurance premium subsidies, supported by global initiatives such as the Global Shield against Climate Risks. This subsidy program is based on a set of principles to guide the design and implementation of appropriate premium subsidies, which evaluates the impact of each dollar of premium on the resilience of poor and vulnerable people. However, the literature is still scant as to which of the financial products, including insurance, or mix of financial products might be the most efficient at protecting vulnerable households against climate shocks.

It may be worthwhile to first return to the foundations of the economics of risk and insurance to inform policy actions for improved financial resilience against climate shocks, including climate risk insurance. The standard literature of economics of insurance has examined the optimal insurance demand of risk averse agents for more than five decades. Mossin (1968) showed that when insurance is costly, it is never optimal to purchase full insurance. Arrow (1965) showed that the optimal form of risk retention is obtained using a straight deductible: if the loss exceeds a pre-defined deductible, an insurance indemnity is paid by the insurer to cover the difference. This classical model of insurance demand relies on its static feature where wealth and consumption are the same, and where the retained loss through self-insurance corresponds to a reduction in consumption.

In the real world, however, households can use (precautionary) savings and/or borrowing to compensate for their losses rather than reducing their consumption. In other words, they can smooth their shocks by reducing their consumption over several periods. This time diversification strategy leads households to be much more risk prone than in the static model. Because of time diversification, the aversion to risk on wealth is smaller than the aversion to risk on consumption. This lower degree of risk aversion for wealth in the multi-period setting translates into lower demand for insurance and lower welfare gain from insurance. This means that self-insurance, or time diversification, is a substitute for market insurance. It is, however, an imperfect substitute because households are impatient to consume; they do not want to smooth their consumption perfectly over time. In addition, they usually face a liquidity constraint; when it is binding, households must absorb their retained losses immediately.

The dynamic demand for insurance and self-insurance can be examined in a simple dynamic financial model, based on lifecycle consumption models with a liquidity constraint. Such a dynamic model can only be solved numerically, so we built a prototype simulation tool to assess the household’s demand for financial services, including insurance and savings, and their impact on the household’s welfare (measured as their certainty equivalent consumption). Although this dynamic financial model is a simplistic representation of real life and has multiple limitations, it can still inform policy actions to improve the households’ welfare by strengthening financial services for climate resilience. The model identifies four key highlights.

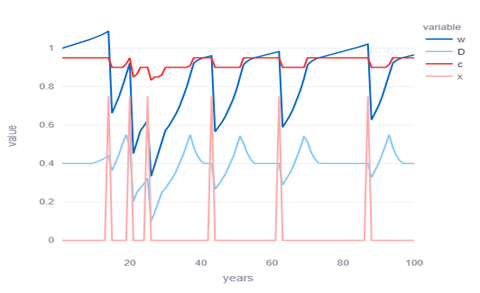

[1] Access to financial services (including savings, credit, and insurance) significantly increases the households’ welfare, and this increase is even larger when households are exposed to catastrophe losses. The households’ demand for insurance and its associated increased welfare can be visualized through the reduction in the volatility of their consumption. Figure 1 below illustrates the impact of climate-related losses (x) on their wealth (w) and on their consumption (c), and the optimal insurance deductible (D) over a 100-year simulation period. In this simulation case, the combination of insurance and self-insurance allows the households to significantly smoothen their consumption over time: the coefficient of variation of wealth is 33 percent while the coefficient of variation of consumption is less than 5 percent. Figure 1 also shows that the demand for insurance increases (that is, the household selects a lower deductible D beyond which losses are fully covered by insurance) when their wealth decreases due to the occurrence of a loss or a series of losses.

Figure 1. The volatility of the household’s consumption reduces dramatically with access to financial services

[2] The value of insurance decreases with the availability of other financial services. When the household is exposed to non-catastrophe losses, access to insurance when other financial services (savings and credit) are already available increases only marginally the household’s welfare: the added value of insurance is low because the household can mostly self-insure such risks. Simulations show that, under a set of reasonable assumptions, access to insurance when savings and credit are already available increases the welfare of the household by about 5 percent. On the contrary, when the household is exposed to catastrophe losses, the value of insurance is much higher, even when other financial services are available. The household purchases insurance to protect against catastrophe losses, which would be too expensive to self-insure. Simulations show that access to insurance can increase the welfare of the households by more than 25 percent.

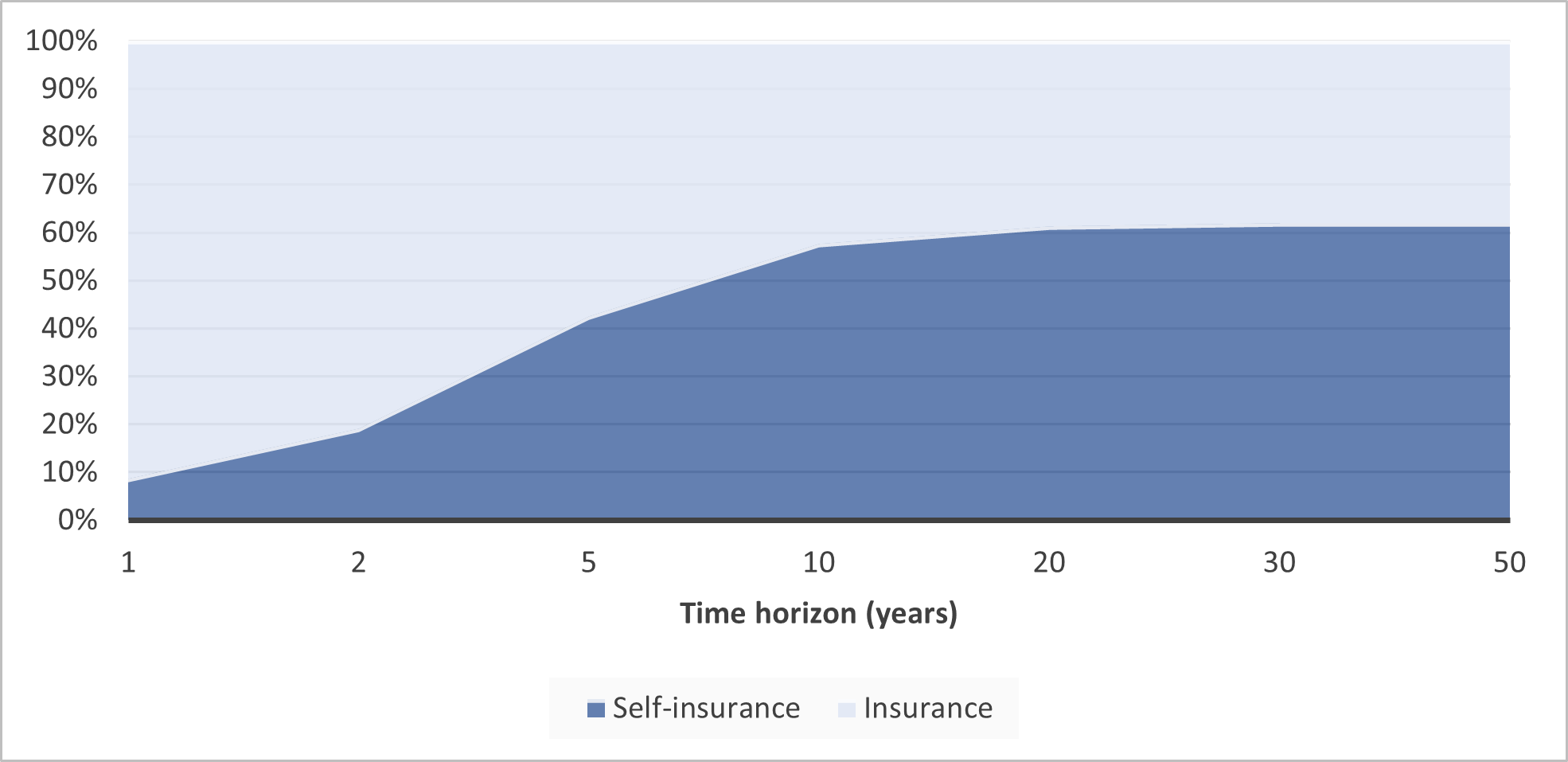

[3] Stable financial markets allow the households to better diversify their risks over time and reduce their demand for insurance. Policy reforms that promote sustainable financial services allow the households to select a longer time horizon in their financial risk management strategy and hence, to better diversify their risks over time, ultimately increasing their welfare. The longer their time horizon is, the higher the level of self-insurance and the lower the level of insurance are. Figure 2 below illustrates the optimal mix of insurance and self-insurance as the time horizon of the household increases: while the households rely mainly on insurance when their time horizon is less than 5 years, they retain more than half of their losses when their time horizon exceeds 10 years.

Figure 2. The demand for insurance reduces with longer time horizon

[4] Public subsidy programs should not be targeted to a specific financial instrument, but rather promote a mix of self-insurance and insurance. Our model shows that public subsidies targeted to insurance are not always the best value for money. Instead, a cost-effective subsidy program should encourage vulnerable households to self-insure small losses through savings and credit, and to insure excess losses through catastrophe insurance (with higher deductible). The optimal mix of subsidies, which maximizes the household’s welfare, depends on the cost of each financial instrument, and the risk profile and preferences of the vulnerable households. Our model shows that, for the same amount subsidies, a subsidy program that allows the households to allocate their subsidies among insurance and self-insurance would increase the household’s welfare by up to 10 percent compared to a subsidy program that would only target insurance.