Budgeting for Resilience: A Blueprint for Incorporating Disaster Risk into Governments’ Budgets

Disasters can wreak havoc on communities and economies. Munich Re reports that natural disasters in the first half of 2023 resulted in enormous economic losses of $110 billion, a third of which was caused by an earthquake in Türkiye and Syria. Estimated economic losses have increased from $52 billion annually in the 1980s to a staggering $228 billion a year over the first three years of the 2020s. As the frequency and intensity of such events continue to rise, governments need to proactively integrate disaster risks into their budgets. In this blog, we highlight some considerations that government officials can take.

Prioritizing Disaster Resilience Amidst Daily Fiscal Challenges

Disasters are contingent liabilities and often a root cause of macro-fiscal shocks . Ministries of Finance are usually called upon to deal with the fallout after disasters by mobilizing funds for relief and recovery or dealing with the ramifications of slowing growth or revenue shortfalls. For example, Türkiye’s Ministry of Finance and Treasury reported that the costs of the most recent earthquake exceeded $100 billion, or 9 percent of GDP. Yet public financial management (PFM) systems are rarely configured for countries to proactively respond to disasters; so, how can we engage with ministries of finance to encourage them to plan for disaster shocks?

We have learned that disaster risk-based budgeting (DRBB), which integrates disaster risk considerations into the government budget cycle, can help with this.

Harnessing the Potential of Disaster Risk-Based Budgeting

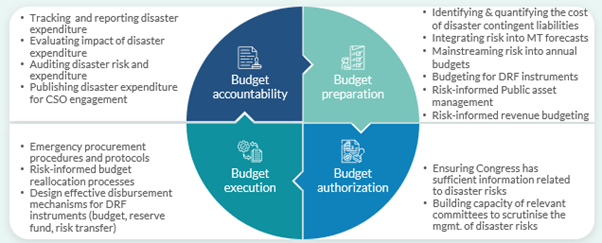

Disaster risk considerations can be amended during budget preparation, authorization, execution, and accountability (see the generic budget cycle as a guide in Figure 1).

For example, disasters can be considered when developing budgets: New Zealand’s National Treasury has included disaster stress tests in long-term fiscal forecasting which sets the stage for its annual budget (see their statement on Long -term fiscal position). The Philippines started considering disaster risk when planning public investments (see the 2022 National Asset Management Plan of the government) (pdf).

After disasters, some regular procurement rules can be amended to allow for quicker procurement to respond to emergencies . Creating clear protocols and guidance in advance can help in making post-disaster procurement more transparent and give implementing agencies the confidence to use the emergency provisions as intended.

At the stage of budget accountability, it is important to ensure that resources are used for their intended purposes in the wake of a disaster when there is often a surge of public expenditure. Tracking post-disaster spending through budget-tagging initiatives or audits of disaster expenditures ensures transparency and facilitates close monitoring of the impact of budget allocations.

Figure 1. Potential entry points for integrating disaster risk into the budget cycle.

Determining Strategic Entry Points for Integrating Disaster Risk Considerations Across the Budget Cycle

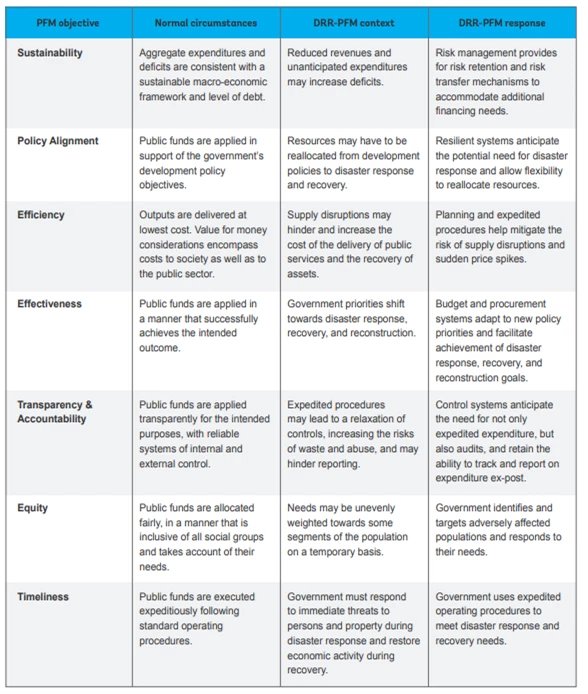

Ministries of finance can lead to integrating disaster risk considerations across the budget cycle, starting with a few entry points to achieve PFM objectives in disaster resilienc e (see Figure 2). Entry points can include addressing context-specific challenges such as agencies not having the right incentives to invest in risk reduction or finance, considering trade-offs in disaster resilience, understanding what role a government’s budget plays in meeting the costs of disasters, and addressing weak accountability related to partial or delayed reporting.

The exact nature of the challenge will determine the appropriate course of action on what PFM system or process needs to change to foster better disaster resilience outcomes. For example, the Department of Budget Management in the Philippines is developing a DRBB framework that identifies priority reforms and activities and action plans on how to implement them.

We are preparing a study with support from the State Secretariat for Economic Affairs (SECO) and FCDO to set out the framework for DRBB. We will share more on this in the coming months, so watch this space and let us know what you think by leaving a comment below.

Figure 2. PFM objectives for disaster resilience